19.7 Forecasting Japanense Car Production

Model 1: Regular OLS Model \[y_t = \beta_0 + \beta_1 t + \epsilon_t\] Model 2: Autoregressive Model \[ y_t = \beta_0 + \beta_1 t + n_t \quad \text{where} \quad n_t = \phi_1 n_{t-1} + \epsilon_t\]

##

## Call:

## lm(formula = cars ~ year, data = jcars)

##

## Residuals:

## Min 1Q Median 3Q Max

## -911.62 -406.49 47.09 353.35 1351.64

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) -924484.82 30143.45 -30.67 <2e-16 ***

## year 471.81 15.25 30.94 <2e-16 ***

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 583.2 on 24 degrees of freedom

## Multiple R-squared: 0.9755, Adjusted R-squared: 0.9745

## F-statistic: 957.1 on 1 and 24 DF, p-value: < 2.2e-16## Series: jcars$cars

## ARIMA(0,1,0) with drift

##

## Coefficients:

## drift

## 452.9600

## s.e. 83.6424

##

## sigma^2 = 182188: log likelihood = -186.37

## AIC=376.75 AICc=377.29 BIC=379.18## Series: jcars$cars

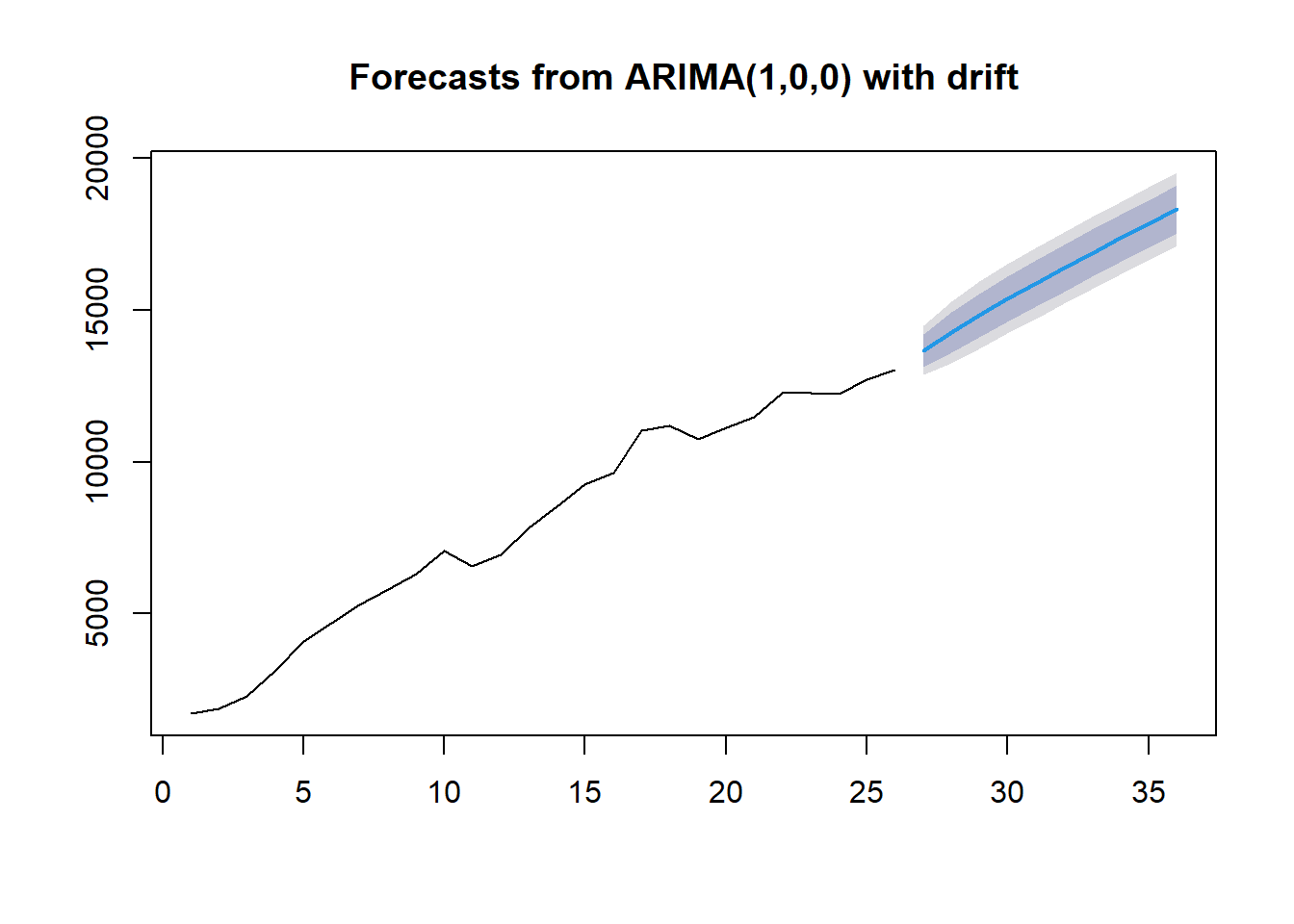

## ARIMA(1,0,0) with drift

##

## Coefficients:

## ar1 intercept drift

## 0.7363 1662.4148 463.5637

## s.e. 0.1347 471.7223 29.2265

##

## sigma^2 = 171700: log likelihood = -192.38

## AIC=392.77 AICc=394.67 BIC=397.8

##

## Training set error measures:

## ME RMSE MAE MPE MAPE MASE ACF1

## Training set 17.28081 389.7285 311.2957 -0.7522648 5.354775 0.5840007 0.1564618