4.5 Types of Budget Authority

Budget authority provided by law is the authority to enter into obligations resulting in immediate or future outlays involving federal government funds. There are multiple forms of budget authority:

Forms of budget authority

Appropriations: Appropriation provides funds for the upcoming year as result of the legislative phase of the budget process. Appropriation acts as a statute providing authorization for federal agencies to incur obligations and make payments for specified purposes. This is the most common mean of providing budget authority.

Authority to borrow: This budget authority provided by law allows the borrowing of funds. Contract authority: Authority provided by law to enter into contracts

Entitlements For programs not covered by the appropriation acts

Not required to go through appropriation process

Spending determined by formula/eligibility requirements (mandatory spending)

- Examples: Medicare, social security, veteran’s benefits

Eligibility criteria established by law

Appropriation Regular

- Annual appropriation

- Multi-year Appropriation

- Advance appropriation

- No year appropriation

- Permanent

Continuing Resolution and Supplemental Appropriation Continuing resolution: Based on spending formula from previous year, which has drawbacks

- Hinder development of new programs in response to changing operating conditions due to restricting operations to previous years level

Supplemental appropriation: Emergency or ordinary

- Requirement of an unforeseen change in operating conditions, e.g., 9/11, financial crisis, COVID-19

- Cost shortfall from previous years appropriations due incorrect projections, e.g., underestimation of medical needs for Veterans affairs

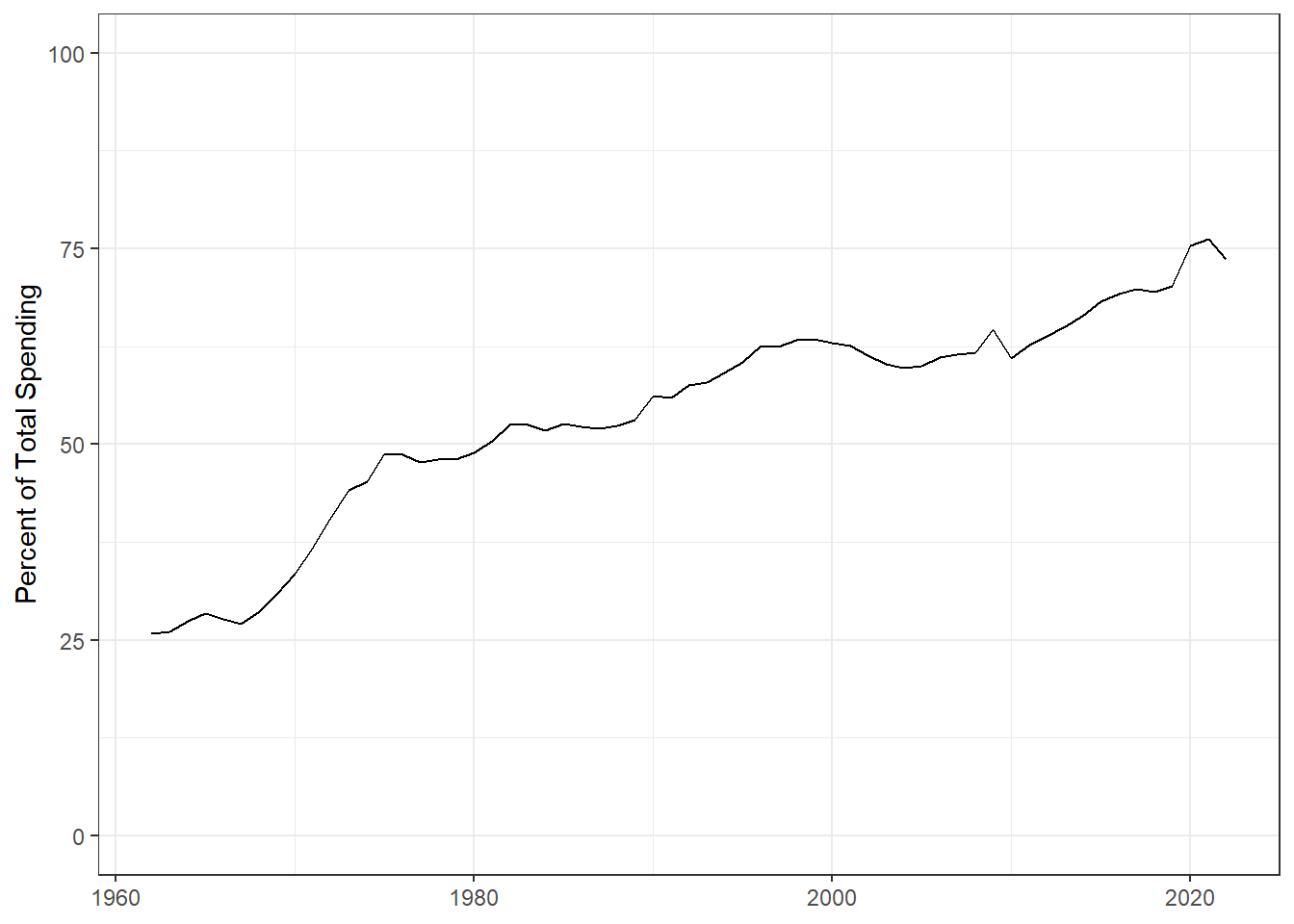

Discretionary and Mandatory Spending Discretionary spending

- Flows through the annual appropriation process with possibility for annual spending adjustments by Congress

- Decreased from approximately 74% of total outlays in 1962 to 26% in 2022

Mandatory spending

- Not part of regular appropriations process

- Control of spending by changing formula to avoid “auto pilot spending”

Means-tested versus non-means test

- Means-tested: Assistance depends on economic status of recipient

- Non-means tested: Assistance is based on demographic or other eligibility, not economic status

CBO: Outlook for the Budget and the Economy

Mandatory Spending over Time