9 Income Taxes

There are three prominent tax bases: Income, consumption, and property. Whereas this chapter presents income taxation, the subsequent chapters cover consumption and property taxes. Note that those taxes are levied mostly at the state and local level since there is neither a sales nor a property tax at the federal level. Keep in mind that with respect to U.S. income taxes, households are taxed and not individuals. The topics covered are (1) Income definition, (2) Income tax components, (3) Evaluation of income tax, (4) Income taxation at the state level, and (5) Corporate income tax. There are also slides and a YouTube video associated with this chapter.

Income taxes are one of the most visible and significant forms of taxation for both federal and state governments, typically structured as a progressive tax. They also serve as an important revenue source for local governments, largely through federal and state aid. Changes in federal income tax policies, such as exemptions or deductions, are often automatically implemented at the state level, impacting state and local revenues. Payroll taxes—another key component—fund Social Security, Medicare, and unemployment compensation.

Prior to 1913, the federal government raised revenue from taxation of goods, i.e., imported products and excise taxes. At the state and local levels, revenue was raised through poll and property taxes. The 16th Amendment from 1909 states the following:

The Congress shall have power to lay and collect taxes on incomes, from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration.

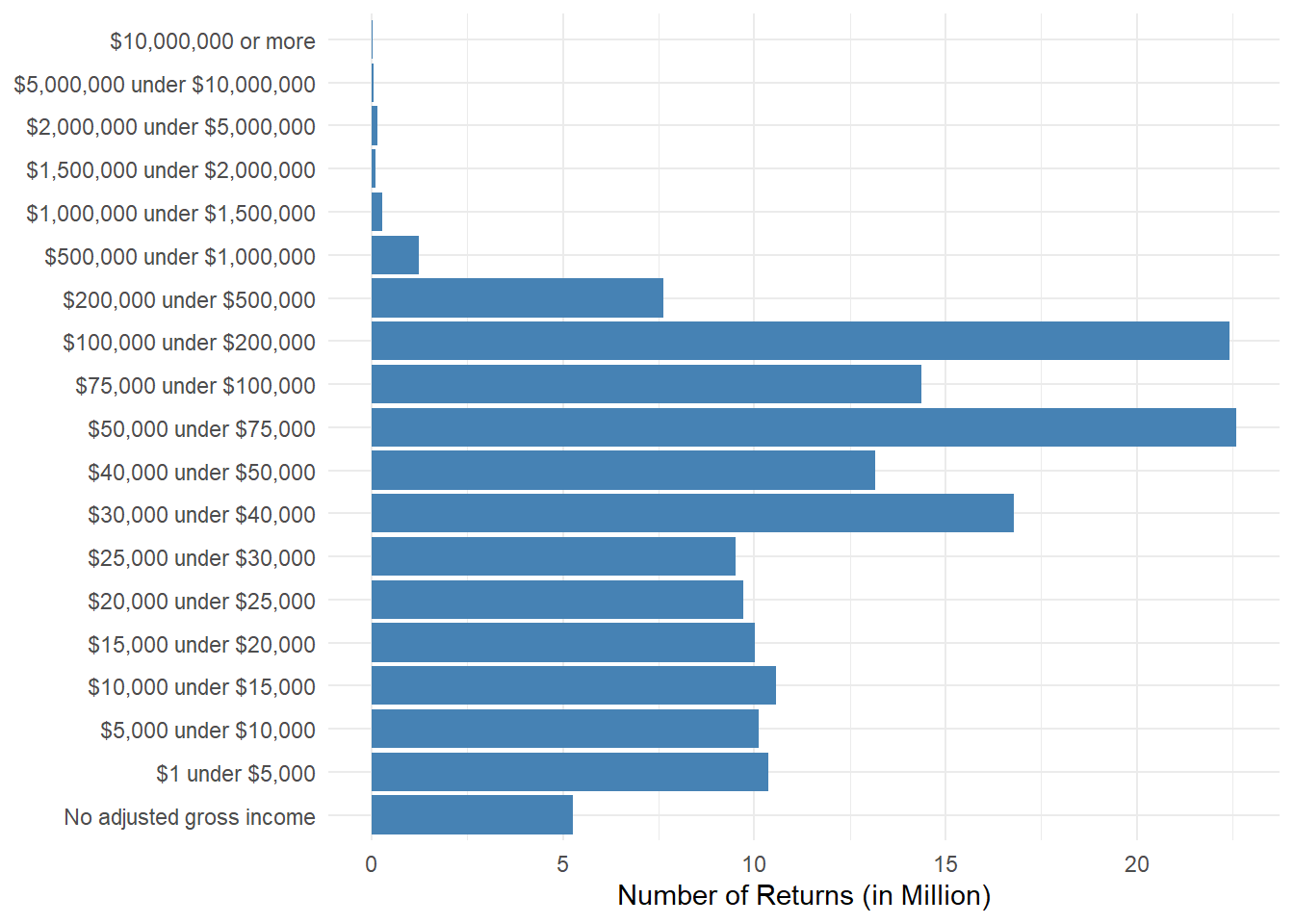

In 1913, the income tax collection obtained tax returns from less than 1% of the population and the tax rate was 1% (See 16th Amendment to the U.S. Constitution: Federal Income Tax (1913)). The figure below is based on IRS Individual Statistical Tables by Size of Adjusted Gross Income 2020

Let us first cover some arguments in favor of and income taxation. On one hand, the income taxation fulfills the tax evaluation criteria of equity since it measures ability to pay. The tax can also be adjusted to the circumstances of the individual household. In addition, the income tax is also adequate with regard to tax yield. That is, if households have increasing incomes (i.e., due to economic growth), government revenue increases as well. The tax base is also very broad allowing for higher amounts of revenue at socially acceptable rates. On the other hand, income taxation has some adverse economic effects since it discourages savings and investment of households because those returns are taxed. Some argue that there is also little association between income taxation and the good and services provided by the government. There is also the argument that the individual income tax is complicated and not very transparent.