4.6 Main Social Insurance Programs

The three main social insurance programs in the U.S. are (1) Old-Age, Survivors, and Disability Insurance, (2) Medicare, and (3) Medicaid.

Old-Age, Survivors, and Disability Insurance (OASDI): This social insurance program is better known under the term Social Security. It is comprised of two trust funds, i.e., Old-Age and Survivors Insurance (OASI) and Disability Insurance (DI). OASI is for retired workers and their dependents as well as the survivors of deceased workers. DI is for disabled workers and and their depedents. Both funds are financed by earmarked payroll taxes (Annual Report)

4.6.1 Medicare

Medicare is a federal health insurance program primarily for individuals aged 65 and older, as well as certain younger people with disabilities. It consists of several parts: Part A covers hospital and inpatient services, Part B covers outpatient medical care, Part C (Medicare Advantage) offers an alternative to traditional Medicare through private plans, and Part D provides prescription drug coverage. Medicare is funded through a combination of payroll taxes, premiums, and general federal revenues.

4.6.2 Medicaid

Medicaid is a joint federal and state program that provides medical care for low-income individuals. Unlike Medicare, it does not have a trust fund and is financed through general federal and state funds. For every dollar a state spends on Medicaid, the federal government provides at least $1 in matching funds, with higher matching rates for poorer states. On average, the federal government covers about 57% of Medicaid costs across all states.

4.6.3 Problems with Social Insurance Financing

Until mid-1980s, handled as “pay-as-you-go”

- Premiums collected this year covered benefits paid this year

Problem: Falling ratio of workers to beneficiaries, i.e., benefits payout exceeding payments

- Reasons: Low birthrates, retirement of baby boomers, low death rates

- 5 workers for each recipient in 1960 and 2 to 1 by 2030

- Increase in health care costs

Possible solution: Actuarial Funding

- Pay into the fund during working years

- Receive principal plus interest upon retirement

CBO Report (February 1996): Mandatory Spending Control Mechanisms

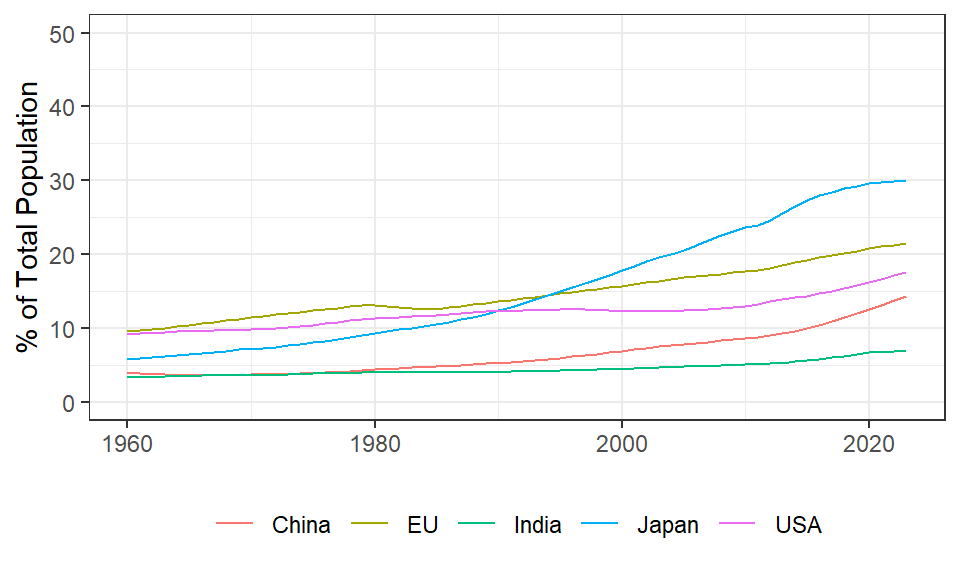

Population Age 65 and over

Actuarial Funding for Social Insurance Programs Establishment of trust funds

- Dedication of payments to fund (payroll taxes) during individual’s working life

- Investment of funds in secure investment vehicles (e.g., U.S. government securities)

- Use of fund’s proceeds (i.e., contributions plus interest earnings) for benefit coverage during retirement

Application

- Possible for Social Security and Medicare: Predictable cycle of work following retirement

- Not possible for Medicaid: No predictable cycle of prosperity and poverty