6.4 Break-Even Analysis

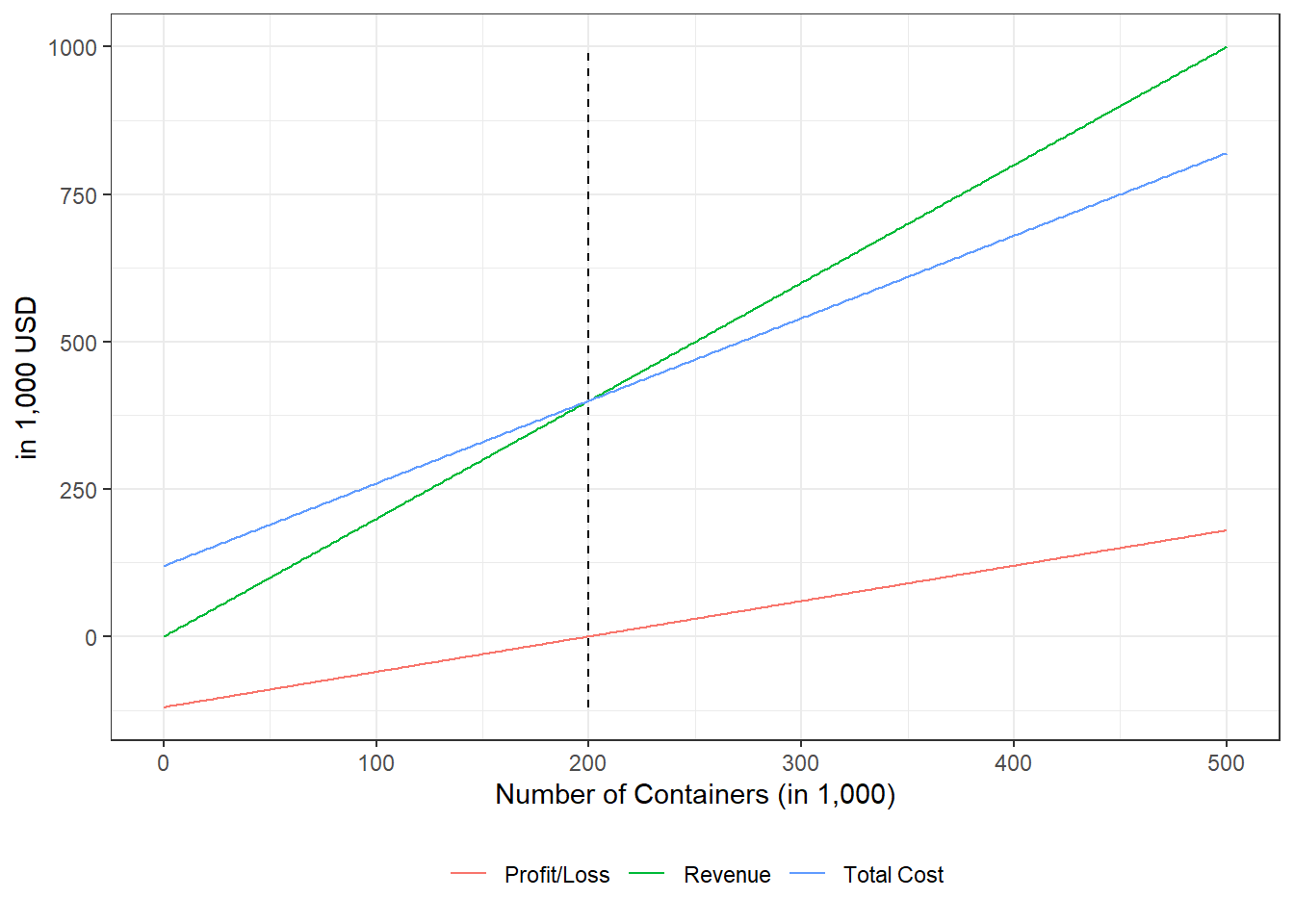

The city department for municipal solid waste (MSW) collection serves about 250,000 households per year who all own one garbage container. The collection fee is $2 per 96 gallon container. Thus, the revenue in this example would be $500,000. On the cost side, we have annual fixed cost that are composed of administrative services ($35,000) and equipment lease ($85,000). The variable cost per container is composed of a landfill charge ($1) and equipment operation on collection routes ($0.40). Suppose that due to inflation, the landfill considers increasing the fee from $1.00 to $1.30 per container. The table below calculates the total revenue, fixed cost, variable cost, and total cost and the old and proposed landfill (LF) fee.

| Item | Current LF Charge | New LF Charge |

|---|---|---|

| Number of containers | 250,000 | 250,000 |

| Collection Fee | $2 | $2 |

| Revenue | $500,000 | $500,000 |

| Administration | $35,000 | $35,000 |

| Equipment Lease | $85,000 | $85,000 |

| Fixed Cost | $120,000 | $120,000 |

| Landfill charge | $1.00 | $1.30 |

| Equipment operating on collection routes | $0.40 | $0.40 |

| Total variable costs per unit | $1.40 | $1.70 |

| Variable Cost | $350,000 | $425,000 |

| Total Cost | $470,000 | $545,000 |

| Surplus/deficit | $30,000 | $(45,000) |

The graph below represents the break even number of containers under the old landfill charge.