8.2 Tax Terminology

Taxes are compulsory payments associated with certain activities (e.g., earning income, owning property, purchasing goods). They reduce an individuals’ ability to allocate resources. Tax policy seeks to achieve that transfer of resources with the least possible economic and/or social harm. Taxes are neither a price for (direct) services received nor a voluntary contribution.

In his book The Wealth of Nations, Adam Smith (1776) establishes the following tax maxims:

- Equity: The subject of every state ought to contribute towards the support of the government, as nearly as possible, in proportion to their respective abilities; that is, in proportion to the revenue which they respectively enjoy under the protection of the state.

- Certainty: The tax which each individual is bound to pay ought to be certain and not arbitrary. The time of payment, the manner of payment, the quantity to be paid, ought all to be clear and plain to the contributor, and to every other person.

- Convenience: Every tax ought to be levied at the time or in the manner, in which it is most likely to be convenient for the contributor to pay it.

- Economy: Every tax ought to be so contrived as both to take out and to keep out of the pockets of the people as little as possible, over and above what it brings into the public treasury of the state.

The following sections cover three important tax aspects: (1) Tax base and tax trigger, (2) Tax rate, and (3) Tax incidence.

8.2.1 Tax Base and Tax Trigger

The tax base refers to the item or economic activity on which a tax is imposed. Common examples of tax bases include income, wealth, and consumption. These form the foundation on which various tax systems are built, allowing governments to collect revenue based on these defined economic activities or assets. Taxation can be categorized as either general or selective. A general tax applies to the entire tax base without any exclusions or deductions. In contrast, a selective tax targets only a specific portion of the base, focusing on particular goods, services, or activities. Indiana sales tax is an example of a selective tax. According to the Sales Tax Information Bulletin 29 (August 2023) by the Indiana Department of Revenue, we have the following:

Generally, the sale of food and food ingredients for human consumption is exempt from Indiana sales tax. Primarily, the exemption is limited to the sale of food and food ingredients commonly referred to as “grocery” food.

The tax trigger is the event or activity that gives rise to the tax liability. This can be determined by the actions of taxpayers, such as earning income or making purchases. Alternatively, the tax trigger can be set by the government, as in the case of property taxes, where the ownership of property creates the tax obligation.

The measurement of the tax base and the determination of tax liability are critical processes in taxation. These involve assessing the size or value of the tax base (e.g., determining the amount of income, wealth, or consumption subject to tax) and calculating the corresponding tax liability based on the established tax rates and rules.

8.2.2 Tax Rates

Tax rate refers to the rate at which the tax base is taxed. In general, the tax rate applied to the tax base determines how much tax is owed. Let us look at income taxes as an example.

The tax base is income, which is adjusted for exclusions, deductions, exemptions, and credits. The next chapter covers the exact mechanics of those items The tax trigger is engaging in an activity that generates income. The tax rate typically follows a graduated schedule, where different portions of income are taxed at varying rates. That is, a graduated schedule involves marginal tax rates that apply to the last dollar of income earned. There is a distinction between the average, marginal, and effective tax rate.

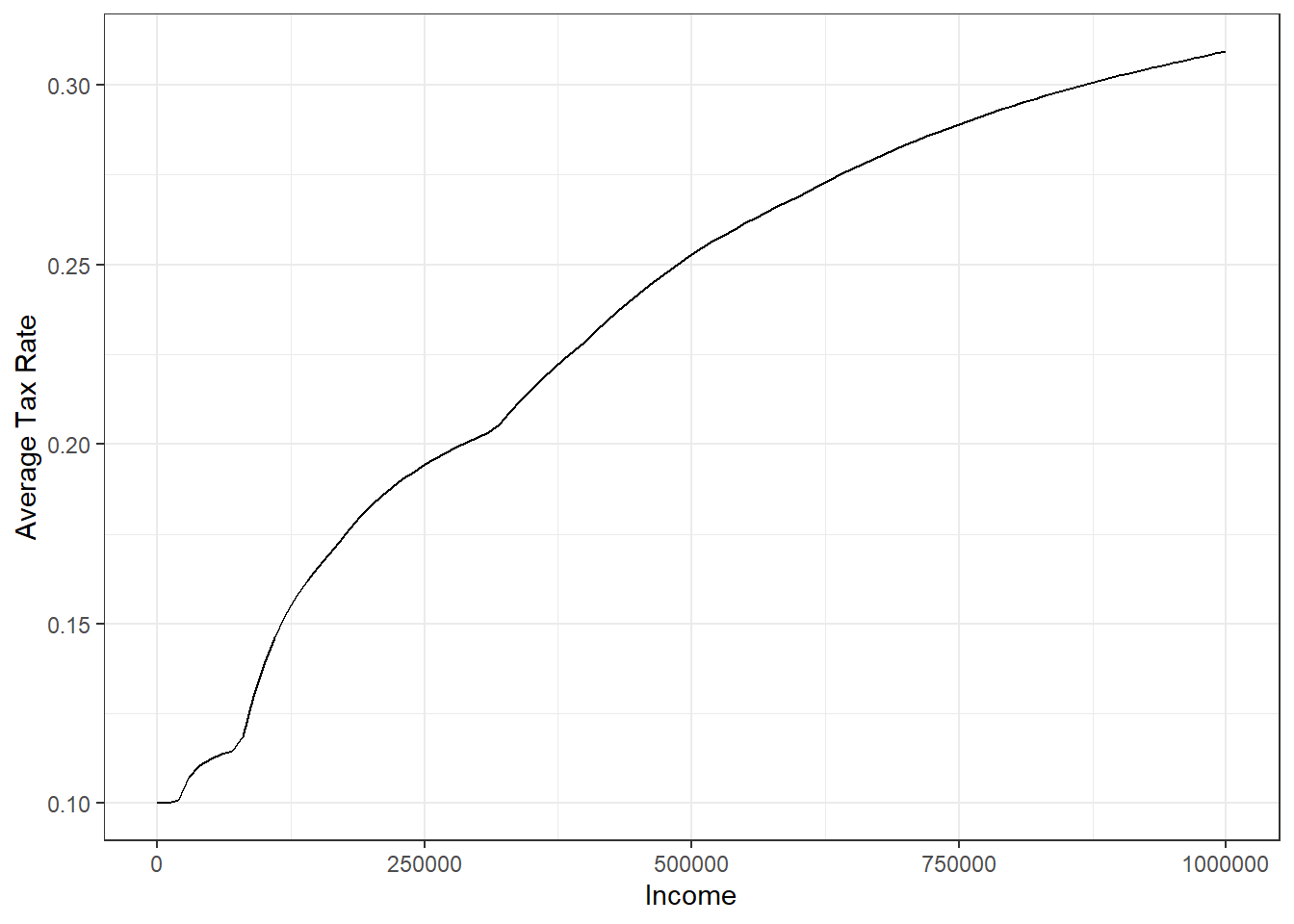

The average tax rate is the total tax collected divided by the dollar value of the tax base, giving an overall sense of the taxpayer’s burden. The marginal tax rate is the change in taxes collected divided by the change in the value of the tax base, showing how much additional tax is paid on the next unit of income. The effective tax rate is the tax collected divided by a measure of ability to pay, such as total income or wealth. This rate is useful in evaluating how taxes impact individuals or entities relative to their overall financial position.

The effective tax rate is often used as an indicator to differentiate between progressive, proportional, and regressive tax systems. For example, in a progressive tax system, the effective tax rate increases with income. In contrast, the effective tax rate remains constant in a proportional tax system, and it decreases with income in a regressive tax system. In the income tax table below, the average and effective tax rates are identical.

| A | B | C | |

|---|---|---|---|

| Income | $10,000 | $40,000 | $100,000 |

| Proportional tax | |||

| Tax amount | $1,000 | $4,000 | $10,000 |

| Effective tax | 10.0% | 10.0% | 10.0% |

| Progressive tax | |||

| Tax amount | $1,000 | $5,000 | $20,000 |

| Effective tax | 10.0% | 12.5% | 20.0% |

| Regressive tax | |||

| Tax amount | $1,000 | $3,000 | $6,000 |

| Effective tax | 10.0% | 7.5% | 6.0% |

Next, consider the following marginal tax rate table. We are going to use this table for the tax calculations that follow.

| Over | But not above | Over | But not above | Tax Rate |

|---|---|---|---|---|

| Single | Married | |||

| $- | $9,525 | $- | $19,050 | 10% |

| $9,526 | $38,700 | $19,051 | $77,400 | 12% |

| $38,701 | $82,500 | $77,401 | $165,000 | 22% |

| $82,501 | $157,500 | $165,001 | $315,000 | 24% |

| $157,501 | $200,000 | $315,001 | $400,000 | 32% |

| $200,001 | $500,000 | $400,001 | $600,000 | 35% |

| $500,001 | $600,001 | 37% |

Let us consider the following situation of a married couple with household income of $137,000. Note that in the U.S., households pay income taxes and not individuals. Based on the above marginal tax rate table, the tax liability is calculated as follows: \[19050 \cdot 0.1+(77400-19050) \cdot 0.12 + (137000-77400) \cdot 0.22= 22019\] The tax liability amounts to $22,019 and the marginal tax rate it 22%. The average tax rate is 16% (i.e., $22,019 divided $137,000).

Figure 8.4: Marginal versus Effective Rate