10.3 Retail Sales Tax

In the U.S., retail sales taxes typically exclude goods used in production for reasons related to economic efficiency, equity, and the promotion of economic growth. The exclusion is meant to prevent the tax from being applied to intermediate goods, which could otherwise lead to a cascading effect and increase production costs. The standards for these exclusions usually involve two criteria: (1) The good must either be a component or physical ingredient of the final product or (2) it must be directly used in the production process.

Sales taxes in the U.S. are often composed of state, local, and special rates. For example, in New York City, the total sales tax is a combination of a 4% state tax, a 4.5% city tax, and a 0.375% surcharge for the Metropolitan Commuter Transportation District (Source). Resources like the Tax Foundation’s data portal provide detailed information on state and local sales tax rates across the country (Data Portal). Sales taxes are not levied in Alaska, Delaware, Montana, New Hampshire, and Oregon.

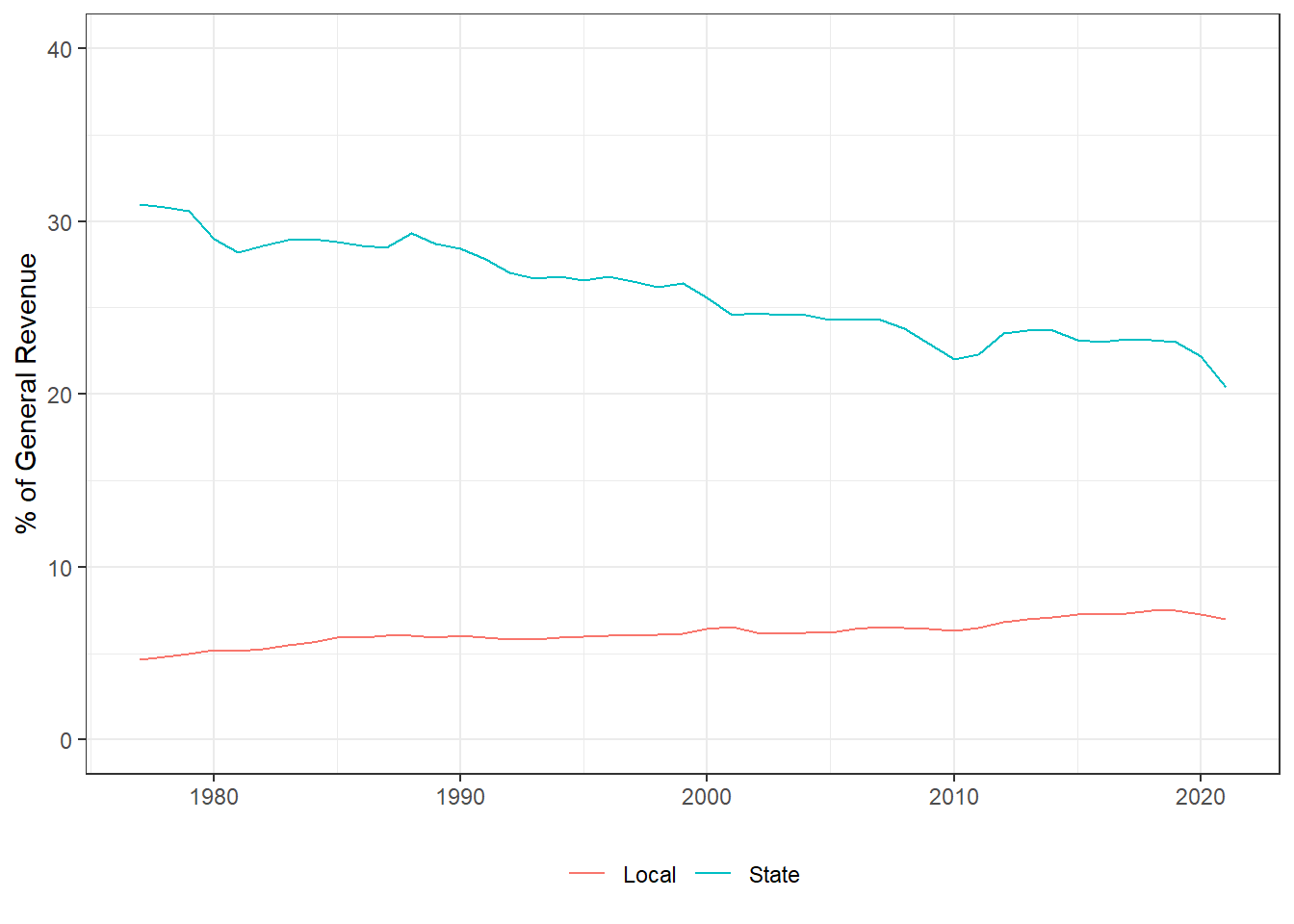

Figure 10.1: Sales Tax Revenue at State and Local Level

Retail sales tax can be either general or selective. A general tax applies to all transactions except for certain exemptions, whereas a selective tax targets only specific, enumerated transactions, such as a lodging tax that applies only to hotel stays. The way rates are applied can also differ, with two primary types: specific and ad-valorem. A specific, or unit tax, is applied based on the number of physical units bought or sold, such as a tax of $0.20 per gallon of gasoline. In contrast, an ad-valorem tax is levied based on the value of the transaction. For example, a lodging tax might be 10% of the total hotel bill, meaning the tax amount fluctuates according to the price paid for the service.